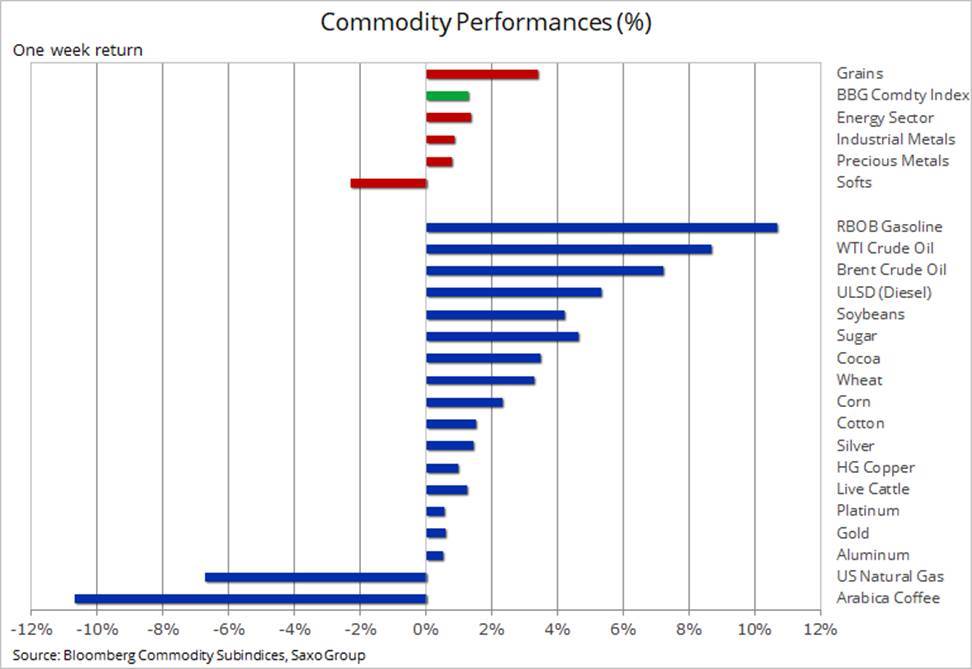

The Bloomberg Commodity Index, which tracks a basket of major commodities spread evenly across energy, metals and agriculture, traded higher for the first time in three weeks. A softer dollar, continued buying momentum among major U.S. crop futures and a Saudi-fueled bounce in oil products, together with Chinese economic optimism all helped support a week of broad-based gains across all three sectors. Gold traded quite passively with ‘algo’ traders currently in charge, something that for now has resulted in an unusually high positive correlation with the movements in the S&P 500 index.

Crude oil and fuel products led from the front as the sector recovered from the recent correction. The OPEC+ meeting saw a strong attack from the Saudi oil minister on members cheating on quotas and shortsellers in the futures market. This follows a week where OPEC, the IEA and BP all warned about a fragile recovery in demand given the continued rise in coronavirus cases around the world.

Gold as well as silver traded slightly higher on the week despite some midweek softness after the FOMC delivered nothing new and U.S. stocks challenged support. While the Fed has promised rock-bottom rates for longer than three years, the initial cross-market reaction with lower stocks and a stronger dollar raised some concerns that the Fed’s tool box has started to look empty, with the element of surprise no longer there.

In a recent update we described gold as looking passive as its movements have been mirroring those seen in U.S. stocks. The lack of fresh input from bonds and the dollar has meant that algorithmic trading systems, often trading correlations between markets, have moved to the driving seat, thereby creating an unusually positive correlation between gold and stocks. Correlations work as a trading strategy to a point. With this in mind, the very short-term direction may be dictated by the stock market.

However, our long-term outlook remains supportive. The combination of inflation protection attracting demand, the outlook for a weaker dollar and the positive views on when a vaccine against Covid-19 will become available are all too optimistic. With these developments in mind and the potential for a very ‘ugly’ U.S. election period ahead, we maintain our bullish outlook for gold. Meanwhile, in the shortterm the performance of U.S. mega-caps and the dollar hold the key to the direction. As a result, we are likely to see the two-month consolidation period being extended further.

Crude oil found a bid following the recent sharp correction and break below the trend that had prevailed since June. Driving the recovery has been upbeat economic data from China and the U.S., the world’s biggest consumers, along with a general improvement in the risk appetite after U.S. mega-cap stocks found support.

Most important, however, was the strong verbal intervention given by Saudi Energy Minister Prince Abdulaziz bin Salman following the OPEC+ meeting this past week. He opened the meeting with a forceful condemnation of members that try to get away with pumping too much crude. He went further during the Q&A session with a journalist by warning short sellers not to challenge the Kingdom’s resolve by saying, “I’m going to make sure whoever gambles on this market will be ouching like hell”.

While potentially a sign of frustration that OPEC+ production cuts have yet to deliver a strong recovery, the minister was probably also trying to prevent increased shortselling amid what OPEC, the IEA and BP call a fragile demand recovery at a time of veryhigh spare capacity and inventories. Since July when fundamentals, but not the price, started to weakenthe gross short held by hedge funds in WTI and Brent crude oil has more than doubled to 235 million barrels.

While short sellers may move the market for a short period of time, fundamentals will always be the main driver. And while the recent 15% correction in Brent crude oil helped to bring the price more in line with current fundamentals, a recovery from here needs more than verbal intervention, despite itcoming from the world’s biggest producer.

We remain cautious about crude oil’s short-term abilityto rally much further unless OPEC+ surprises the market in abandoning its planned 2 million barrels/day production increase set for January. While the U.A.E., a major laggard in August, will cut production again, some concerns linger with regards to Iraq and Libya. Iraq has, according to tracking data, increased its production this month while Libya’s ceasefire may support a recovery from the current sub-100,000 barrels/day of production.

U.S. natural gas slumped back below $2, a seasonal low going back almost 20 years. Lower demand triggered by lockdowns and Hurricane Sally disruptions impacting both demand and exports helped drive a bigger-than-expected weekly inventory build. In early trading on Friday the price found support at the key $1.94 level, but nervous trading probably will persist ahead of the annual turnaround from the injection to winter extraction season, when demand for heating exceeds production.

Soybeans look set for a sixth weekly gain as China continues to step up purchases after adverse weather these past few months damaged crops in some areas of the country. According to the U.S. Department of Agriculture, soybean sales in the season that started September 1 have reached a record 30 million metric tons, with more than half going to China. During the past week it broke back above $10/bu to the highest level since May 2018.

With corn prices on the Dalian exchange in China reaching a five-year high, the demand for U.S. corn has also been solid with the price in Chicago rising to a six-month high. On September 23, Chinese customs will publish monthly data on agricultural imports. With the trade deal under increased scrutiny the data will be watched closely, also in order to determine the potential for further price gains just before a large U.S. crop is harvested.