Saudi Arabia News

- The online grocery delivery penetration, basis users, is expected to reach 20% by the end of 2025.

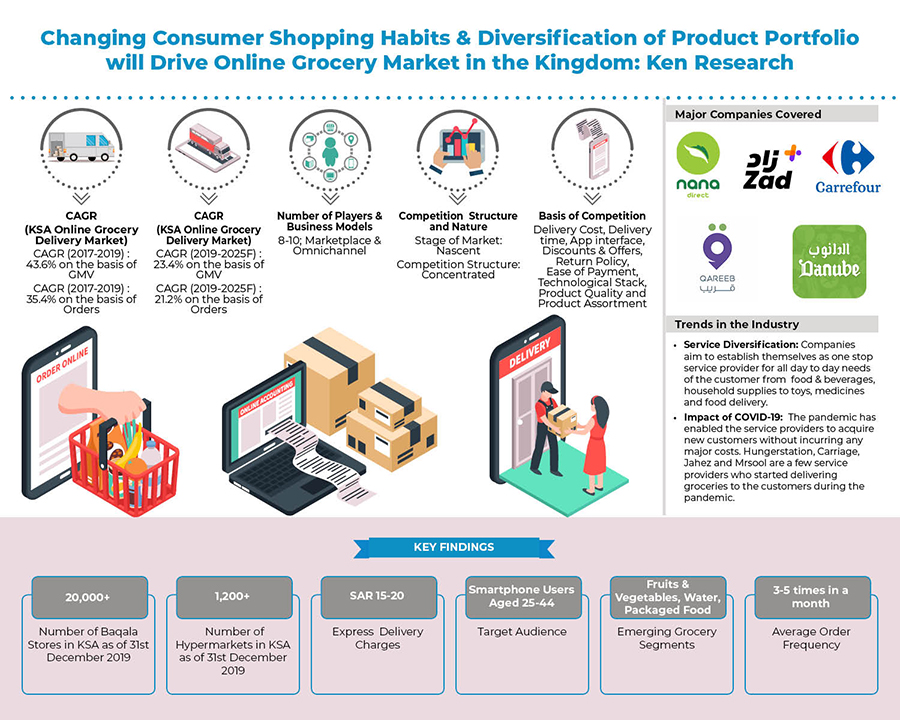

- The demand for expresses delivery is expected to grow at a CAGR of 32% between 2019 and 2025. The charges for express delivery are expected to decline by the end of 2025.

- Technological developments such as drone deliveries, warehouse automation and voice ordering are anticipated to be adopted by service providers to enable quicker deliveries.

Diversification of Product Portfolio: Companies aim to establish themselves as one stop solution for all day to day needs of the customer. They have been focussing on diversifying their product portfolio from food, beverages, fruits, vegetables to household supplies, beauty & health, medicines, toys, food and delivery of other daily needs of a family.

Impact of Covid-19: Due to COVID-19 Outbreak, people avoided crowded places and turned to online grocery shopping amid escalating fears. Major product categories witnessed growth between 20-40% during the pandemic such as water, personal hygiene, home cleaning, fruits & vegetables. March and April was marked by a huge gap between demand and supply as no one was prepared for this situation in advance therefore companies faced logistical challenges. Average delivery time also increased from one to three days to one to two weeks. In order to fulfil the increased demand, companies expanded their delivery fleet by partnering with third party delivery companies to manage last-mile logistics.

Expanding Partnerships with Third Party Operators: It is anticipated that companies would be expanding tie ups with suppliers & grocery stores, food delivery companies, e-wallet companies to leverage their capabilities to fulfil customer orders. Companies are also expected to establish dark stores across the Kingdom to ensure quicker and efficient logistics management.

According to the report by Ken Research titled "KSA Online Grocery Delivery Market Outlook to 2025- Driven by Regional Changing Shopping Habits of Consumers and Expansion of Local and International Players in the Kingdom" the Online Grocery Delivery Market will be valued at SAR 650 Billion by the end of 2025, registering a CAGR of 23.4% between 2019 and 2025. The market will witness growth owing to rise in investment in marketplace companies & innovative strategies adopted by service provides.

Key Segments Covered:-

- By Region

- Central

- Western

- Eastern

- Southern

- Northern

- By Product Category

- Food & Beverages

- Fresh Food

- Household Supplies

- Beauty and Health

- Others

- By Mode of Payment

- Cash on Delivery

- Pre-Delivery Online Payment

- Card on Delivery

- By Delivery

- In a Specific Time Period (Same Day or Next Day)

- Express Delivery (30 minutes-2 hours)

- Other (2-3 Days or More)

- By Age Group

- 18-24 years

- 25-34 years

- 35-44 years

- 45+ years

- By Gender

- Male

- Gender

Companies Covered:-

- Nana Direct

- Zadfresh

- Carrefour

- Danube

- Qareeb.com

Key Target Audience:-

- Online Grocery Delivery Companies

- Supermarkets & Hypermarkets

- E-commerce Companies

- Food Delivery Companies

- Investors and Venture Capitalists

- Logistics Companies

- Government Organization catering to the FMCG Industry

Time Period Captured in the Report:-

- Historical Period: 2017–2019

- Forecast Period: 2020-2025

Key Topics Covered in the Report:-

- Difference between Online & Offline Grocery Shopping. Why Online Grocery is the Way Forward?

- Target Addressable Audience

- Supply Ecosystem and Competition Parameters

- Demand Scenario, Target Customer and Factor Influencing Consumer Behaviour

- Process of On Boarding a Grocery Store

- Role & Responsibilities of Company and Partner Grocery Store

- Gaps & Possible Solutions of Managing Logistics

- Factors Influencing Customer Behavior

- Seasonality Trends

- Features of a Grocery Delivery Application

- Technologies Facilitating Online Grocery Delivery Industry

- Upcoming Technologies in Online Grocery Delivery Industry

- Future Market Trends and Way Forward

- Marketing Strategies

- Industry Best Practices

- Covid-19 Impact on KSA Online Grocery Delivery Market

- Analyst Recommendations

- KSA Online Grocery Delivery Market

- KSA Online Grocery Market

- KSA Online Grocery Orders

- KSA Online Grocery Average Order Size

- Riyadh Grocery Market

- Jeddah Grocery Market

- Medina Grocery Market

- Online Grocery Food and Beverage Orders

- Online Grocery Household Supplies Orders

- Online Grocery Fresh Food Orders

- KSA Online Grocery Delivery Charges

- KSA Online Grocery Express Delivery

- KSA Online Grocery Users

- Marketplace Grocery Companies KSA

- Pureplay Grocery Companies KSA

- Omnichannel Grocery Companies KSA

- KSA Online Grocery Delivery Time

- COVID-19 impact KSA Online Grocery

- Carrefour Online Grocery Orders KSA

- Zad Online Grocery Orders

- Danube Online Grocery Orders

- Qareeb Online Grocery Orders

- Nana Direct Online Grocery Orders

- Amazon Online Grocery Orders

- Logistics Cost Online Grocery KSA

- Commission Online Grocery KSA

- Online Grocery Future KSA

For More Information on the research report, refer to below link:-

KSA Online Grocery Delivery Market Outlook

Related Reports:-

Gaps in offline grocery shopping such as the inconvenience of commute, long payment queues, and cost of impulse buying led to the introduction of e-grocery delivery in the UAE. Population aged between 25 and 44, is considered an influential customer base for online grocery shopping. The industry is currently positioned in a growth stage registering a double-digit growth rate close to 31% between 2016 and 2019. High internet penetration, rising working population, and an increasing number of single families have led to the growth of e-grocery services in the UAE. The number of companies offering grocery delivery services in the UAE has increased over the years. Companies have expanded their product portfolios from food & beverages to household supplies, baby food, fresh food, fish & meat, and other product categories.

UK online retail market grew at double digit growth rate in terms of GMV over the review period 2013-2018. The market growth was supported by the increase in total smartphone penetration, growth in online shoppers and rise in youth population. The availability of better deals and offers along with change in consumer behaviour towards in-store has significantly affected the growth in the market and has changed the digital landscape in the industry. The market is currently placed in the growth stage owing to the increasing penetration of online retail sales during 2019. As more retailers turn online for their shopping, more and more shops are leaving the high street (i.e. offline stores in UK). On the other hand, online retail players have become highly competitive on the basis of personalized experience and social engagement.

Taiwan’s online retail market grew at the single-digit growth rate in terms of GMV over the review period 2013-2018. The market growth was supported by the increase in total smartphone penetration, growth in online shoppers and a rise in the urban population. The availability of better deals and offers along with a change in consumer behavior towards in-store has significantly affected the growth in the market and has changed the digital landscape in the industry. Apparel and Footwear dominated the online retail market as they have the highest demand among both male and female populations while home care being largely saturated and highly competitive, accounted for the lowest revenue share. The competition in Taiwan online retail market has increased over the years leading to the increasing number of online retail websites in Taiwan. Major companies include Momo shop, Fubon Group, Yahoo!, Sea Ltd., President Chain Store Corp., Apple, Mega Co. Ltd., Eastern Media International Corp., and several others are competing by providing the all device optimization, better deals, hyper-personalization through personal engagement and convenient, secure and fast payment modes. The online retail market in Taiwan is expected to witness a single-digit growth rate in the forecast period 2018-2023E. The market will increase at a declining rate as is expected to move gradually towards its maturity stage. Taiwanese population still prefers to shop offline owing to certain trust issues, issues related to cybersecurity, lesser regional presence of online retail companies and others.