Corporates understand the vital importance of becoming more sustainable, both to unlock growth and to create corporate strategic advantage. Meeting this sustainability challenge requires three building blocks – technology, scale-up capabilities, and capital all working together to start the flywheel spinning, as outlined in a recent Arthur D. Little Prism article. Previously, capital has often been lacking for quick and impactful breakthroughs, but now the range, options, and availability of green finance forcorporates are increasing rapidly, helped by historically low interest rates, a greater investor appetite for risk, and expanded and more sophisticated subsidies and government incentives. Options span traditional and innovative green financing methods, both for the funding of green assets and technology development.

Corporates may learn from techniques that have evolved within sustainable finance to support the scale up of clean technology. This Viewpoint explains the green financing landscape and how to determine the best option for your needs.

Previously, transformational change in sustainability was limited due to a lack of available funding to support often long and costly innovation roadmaps. Without funds, corporates cannot successfully leverage the existing building blocks of winning technology and scale-up capabilities. While investors have increasingly considered green opportunities (with a record US $580 billion of global climate finance flows in 2019, according to the Climate Policy Initiative), there has been a mismatch between their priorities and the available options.

Four trends have transformed this picture over the last year:

1. Increased government action, through greater regulatory activity and focus on building back greener post-pandemic economies. Billions of dollars of funding have been made available by initiatives such as the EU Green Deal and national and supranational organizations such as export credit agencies and development banks – but only to projects that demonstrate a positive impact on sustainability.

2. Greater investor interest in, and funding for, green initiatives. These allocations are often coupled with an appetite for higher risk opportunities in an era of low returns from other asset classes.

3. Higher involvement of industrial companies. Corporates are becoming more familiar with the breadth of potential green technologies to adopt and are increasingly looking at novel financing routes to enter the market or scale up their ambitions to meet sustainability and net zero objectives.

4. Rapidly widening ecosystems. Green innovation is transforming the traditional ecosystems corporates operate in, bringing new players, partners, and opportunities for collaboration. A good example is the Alliance to End Plastic Waste, a nonprofit founded by companies that make, use, sell, process, collect, and recycle plastics. Its members aim to invest $1.5 billion over five years to develop solutions that minimize and manage plastic waste, to catalyze additional investments, and to promote solutions such as reuse, recycling, and recovery.

The green finance ecosystem

Corporates looking to leverage green investment now have a widening choice of both traditional and innovative green financing options available to them, backed by greater capital from multiple private and public sources. To explain the ecosystem and its players, we have split these options into two categories:

1. CAPEX funding of assets (e.g., a wind farm or a plastics recycling facility).

2. DEVEX funding of new technology until first commercial construction (e.g., next-generation solar technology or the development of new plastic recycling processes).

The green financing radar (see figure overleaf) illustrates how private and public funding may complement corporates in financing green innovation ecosystems. (Note that investor categories are diverse, and relative positions may vary widely.)

Aimed at both developing and mature investors, they provide focused funding for projects that were previously overlooked. However, due to their niche nature, blue bonds can be difficult to incorporate into wider investor approaches, leading them to be bypassed in favor of other options.

■ ESG-linked finance. As well as green/blue loans/bonds related to a specific project/purpose, there is a growing number of ESG-linked loans/bonds. Here funding is not linked to a specific purpose, but ESG KPIs are defined and if they are met the interest rate reduces.

Asset recycling platforms

Proven options from capital-intensive clean infrastructure:

Across both categories, risk appetites and the players themselves vary, depending on investment horizons, asset maturity, and technology readiness levels (TRLs). For example, early-stage, high-risk DEVEX funding often comes from government grants or seed funding. When the technology develops, it attracts venture capital backing before appealing to lower-risk investors such as private equity in its mature

phase. These investors come into play in midrange commercial readiness stages once technology risks and early commercial hurdles (such as proof of market viability) have been overcome.

Innovative green asset financing options

Alongside traditional funding options such as debt or equity investment, project financing, and the creation of investment funds and trusts, there is a growing range of innovative green financing options for corporates and large family offices looking to accelerate green projects and technology, provided by specialists and, increasingly, by commercial banks. Focused on sustainability, these include:

Sustainable bonds

■ Green loans/bonds. Also known as climate bonds, these are long-term fixed-income financial instruments that have positive sustainability, environmental, and/or climate benefits. Aimed at mature investors, they raise finance for climate change solutions and projects.

On the positive side they increase the funding available for green projects but bring higher levels of project scrutiny. Demonstrating their growth, 39 bonds were issued in 2020 through the London Stock Exchange green bonds initiative, raising $18 billon.

■ Blue loans/bonds. These bonds focus solely on raising finance for certified and tracked solutions and projects within the blue economy, assisting better stewardship of oceans and associated industries. For example, the Seychelles government issued a $15 million sovereign blue bond.

■ Capital recycling. An emerging vehicle, capital recycling repurposes funds toward greener initiatives by selling or leasing an entire asset (or a stake in it) when it reaches a lower risk phase. The capital is then recycled by investing in new green projects. For example, a wind farm developer could sell a stake in a specific project to a mature investor, such as a corporate infrastructure company or government, when it begins operations.

Capital recycling unlocks new funding for green projects, although asset control is lost and there can be sensitivities if released funding is not used for green projects or assets are transferred from the public to private sector.

■ Farm down. Also known as "asset rotation" or "build-sell- operate," equity stakes in a project are sold progressively to long-term investors, such as investment funds, investment banks, or private investors. This reduces CAPEX and the investment burden on project developers building clean energy infrastructure while delivering stable, ongoing returns for investors.

As with capital recycling, this results in the loss of control of the underlying asset and can lead to systemic risk if multiple investors rely overly on the investment returns generated by infrastructure assets. An example is EDP Renewables’ $975 million asset rotation deal for European wind farms.

■ Asset platforms (or yield companies). An asset platform is a listed or unlisted company formed by a group of investors to own green, de-risked operating assets that produce a predictable cash flow and returns, primarily through long- term contracts. Investors include corporate companies with an energy/renewables focus, investment managers, and investment banks. A successful example is NextEra Energy Partners.

Asset platforms provide corporates with a high price for their developed, mature assets while retaining greater value compared to simply selling them off. However, yield cos

have a need to continually acquire new assets and require frequent access to capital to fund growth and investor distributions. Listed yield cos must also meet additional compliance and corporate guidance regulations.

■ Special purpose acquisition companies (SPACs). A SPAC is a company formed and funded via initial public offering (IPO) solely for the purpose of acquiring a target company, which it then takes public. This dramatically shortens the route to IPO (from one to two years to five to six months) while raising funding for capital-intensive startups.

Founders, early investors, and corporates benefit from earlier, profitable exits, while still retaining upside potential. For example, electric utility Engie decided to spin out EVBox (a startup specializing in electric vehicle [EV] charging, which it acquired in 2017) publicly via a SPAC. At a valuation in excess of $1.4 billion, this transaction will allow Engie

to monetize its investment returns much sooner than otherwise possible.

SPACs raised over $80 billion in 2020 alone, with a particular focus on acquisitions in the energy, tech, and EV/battery sectors. However, SPACs are higher risk and are normally pre-profit – not always an easy fit with the expectations of investors in listed companies. The currently saturated market also means SPACs are chasing fewer viable investment opportunities and may need to return cash to shareholders instead.

Technology financing options

Corporates looking at investment options for DEVEX financing can access a wide range of potential sources, depending on the TRL of their project. That makes it key to select the right partners for the right stage when it comes to investment in the TRL journey, and particularly vital to understand how nontraditional partners, such as investors, can assist.

Along the TRL curve and time horizons, potential investment partners and green opportunities for corporates include:

■ Government/public funds, delivering early-stage grant investment and support for innovative projects. For instance, the EU’s Just Transition Mechanism supports and provides grants, loan facilities, and private investment.

■ Government-backedventurefunds, providing investment into green technology ventures complementing private venture capital. The European Circular Bioeconomy Fund, for example, is backed by the European Investment Bank

and aims to be an important financial instrument in achieving the European Green Deal goals of making Europe climate neutral by 2050.

■ Venture capital and other early-stage investors, typically aimed at equity financing for startups and emerging companies with high-growth potential.

■ Institutional investors, such as commercial banks and pension funds, also play an important role. Large players such as Norway’s sovereign wealth fund and US-based asset manager BlackRock explicitly promote sustainable investment.

■ SPACs, providing large-scale funding for innovative technologies.

■ Industrials, working with companies within the supply chain to share risk and investment by pooling funds and building consortia. For example, Dow, LyondellBasell, and NOVA Chemicals created the Closed Loop Circular Plastics Fund to invest in scalable recycling technologies, equipment upgrades, and infrastructure solutions.

Success factors

Adopting the right green funding option will of course vary depending on an individual corporate’s requirements, objectives, and circumstances. However, corporates can learn from the experience of other sectors when it comes to sustainability finance. Whichever options are chosen there are three common key success factors:

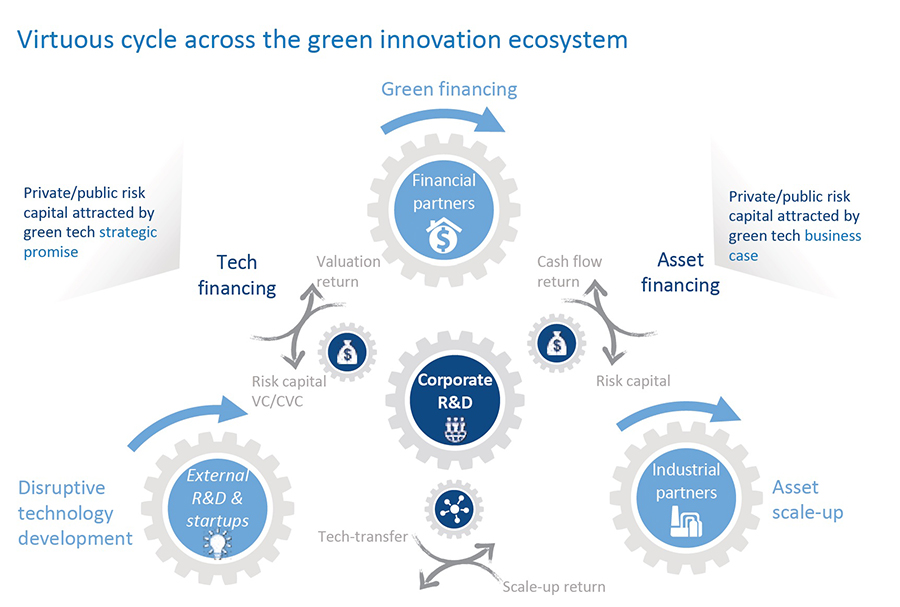

1. Solution ecosystem. Green technology ecosystems bring together a widening number of partners, often from previously unconnected industries and technologies. Corporates therefore need to create a sustainable ecosystem that brings together technology, scale, and capital to spin the flywheel (see figure below) and achieve their investment aims. Large, diversified companies will typically participate in two or more such ecosystems. In some, they may be enablers or contributors, such as with a new recycling technology. In others, they will need to co-initiate and orchestrate to realize their strategic ambitions and extract maximal value.

- Government/public funds, delivering early-stage grant investment and support for innovative projects. For instance, the EU’s Just Transition Mechanism supports and provides grants, loan facilities and private investment.

- Government-backed venture funds, providing investment into green technology ventures complementing private venture capital. The European Circular Bioeconomy Fund, for example, is backed by the European Investment Bank and aims to be an important financial instrument in achieving the European Green Deal goals of making Europe climate neutral by 2050.